Analysis of first quarter 2018 financial data

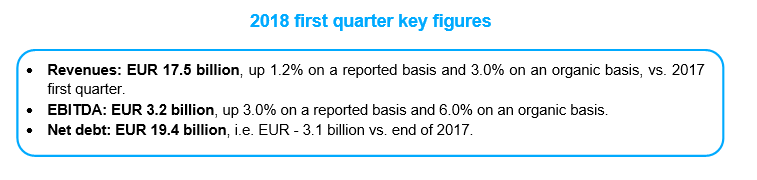

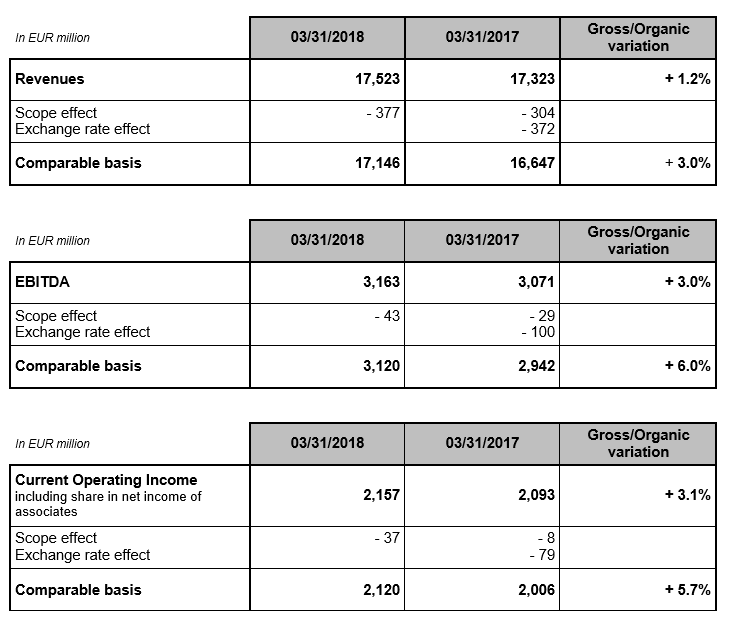

Revenues of EUR 17.5 billion

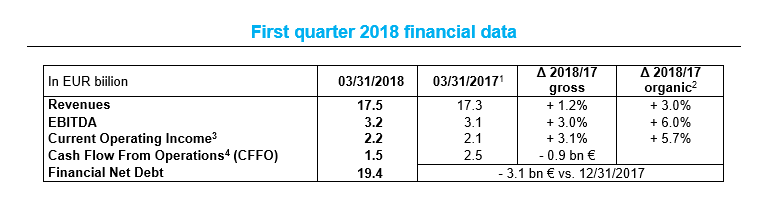

Revenues as of March 31, 2018 reach EUR 17.5 billion, up 1.2% on a gross basis and 3.0% on an organic basis.

This growth is substantially explained by the strong increase in renewable power generation in France and in Belgium, by the increase of gas and electricity sales in the retail segment in France, by the commissioning of assets in Latin America and by the favorable temperature impact for gas distribution in France. It is also driven by recent acquisitions, including new contributions from two hydroelectric power plants in Brazil, the Talen services company in the United States and Keepmoat Regeneration, the leading provider of regeneration services in the United Kingdom.

These effects are partially compensated by a negative foreign exchange impact, in particular attributable to the Brazilian real and the US dollar vs. Euro, by less favorable market conditions for thermal activities in Europe in 2018, by a decrease in achieved prices of nuclear and hydroelectric production in Belgium and France, and by the scope out effect of disposals (in particular thermal assets in Australia, in Poland and in the United Kingdom).

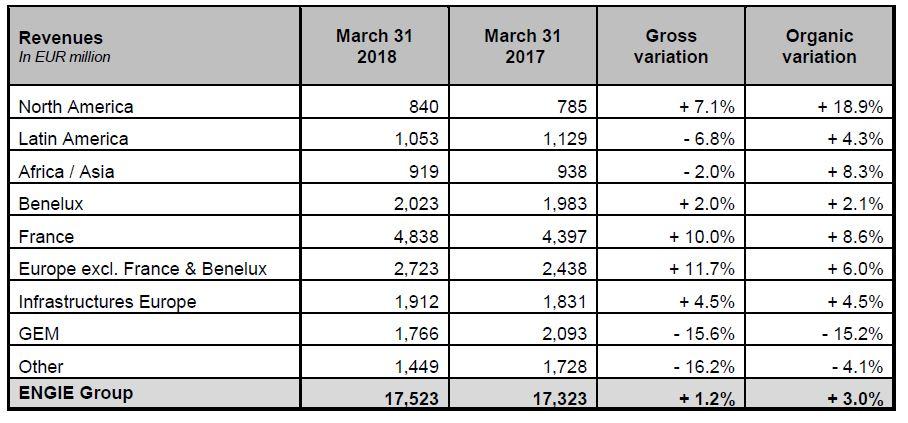

More details on the evolution of the revenues by reportable segment are available on pages 7 and 8.

EBITDA of EUR 3.2 billion

EBITDA for the period amounts to EUR 3.2 billion, up 3.0% on a gross basis and 6.0% on an organic basis, mainly for the reasons mentioned above. In addition, the sharp increase in EBITDA is also due to a 30 basis points increase in service activities margins and to the outstanding performance of midstream gas activities in a favorable market environment in Europe.

EBITDA performance is contrasted among segments:

- EBITDA performance is contrasted among segments increases sharply due to the sound performance of renewable activities in Canada and the positive temperature effect in the United States.

- EBITDA for the Latin America segment is slightly down on a reported basis due to a negative foreign exchange impact of the Brazilian real and the US dollar vs. Euro, partially offset by the additional contribution of the two hydroelectric power plants in Brazil (Jaguara, 424 MW and Miranda, 408 MW). Organic growth is significant and explained by the commissioning of wind (Santa Monica, 97 MW) and solar (Assu, 30 MW) assets in Brazil as well as by tariff increases in gas distribution in Mexico and Argentina.

- EBITDA for the Africa/Asia segment is significantly declining because of a negative foreign exchange impact of the Australian dollar, the US dollar and the Thai baht vs. Euro, the scope-out effect resulting from the disposal of the Loy Yang B coal plant in Australia in January 2018 and the closure of the Hazelwood coal plant in the same country in March 2017. These effects are partially offset by thermal generation in Thailand and Turkey and by higher power prices in Australia.

- EBITDA for the Benelux segment is stable. “Lean 2018” performance plan effects and the good performance of gas and electricity sales activities and renewable power generation in Belgium are offset by the decrease in EBITDA of the nuclear power generation activities due to lower volumes (ca. - 4%) and lower achieved prices.

- EBITDA for the France segment is strongly increasing due to higher wind and hydro power generation and to higher heat sales linked to the positive temperature effect. These positive effects compensate a temporary downturn in retail sales margins, this downturn being due to increasing prices of Energy Savings Certificates (Certificats d’Economie d’Energie) that will be eventually passed through to final customers. This performance for B2C activities in the first quarter does not reflect the expected dynamics for the full year.

- EBITDA for the Europe excluding France and Benelux segment is declining. This is mainly explained by lower distributed volumes and by a decrease in distribution regulated rates in Romania since April 2017, by the disposal of distribution activities in Hungary in January 2018 and by a negative foreign exchange impact of the British pound and Romanian leu vs. Euro. These effects are partially offset by the acquisition of Keepmoat Regeneration (buildings regeneration in the United Kingdom) and the launch of energy sales retail business in June 2017 in the United Kingdom.

- EBITDA for the Infrastructures Europe segment is slightly down, mainly resulting from lower storage capacity sales combined with the negative impact of tariff revisions for gas transport infrastructures and LNG terminals, in France, which partially offset the favorable temperature effect.

- EBITDA for the GEM (Global Energy Management) segment is sharply increasing, mainly benefitting from the good performance of midstream gas activities in a favorable market context in Europe in 2018, while the first quarter of 2017 was impacted by challenging gas sourcing conditions in the south of France.

- EBITDA for the Other segment is down on a gross basis after the disposal in 2017 of thermal power generation assets in the United Kingdom and in Poland. On an organic basis, the decrease is due to lower downstream activities of gas and electricity sales to small businesses in France and very favorable market conditions in 2017 for thermal activities in Europe.

Current operating income of EUR 2.2 billion

Current operating income reaches EUR 2.2 billion, up 3.1% on a gross basis and 5.7% on an organic basis compared to the end of March 2017, for the same reasons as for EBITDA, as depreciation remains stable versus the first quarter 2017.

Financial net debt of EUR 19.4 billion

As of March 31, 2018, net financial debt reaches EUR 19.4 billion, down EUR 3.1 billion from year-end 2017, mainly due to the effects of the portfolio rotation program (EUR - 2.6 billion) namely with the closing of the disposal of Exploration & Production activities in February 2018.

Cash Flow From Operations (CFFO) stands at EUR 1.5 billion over the first quarter of 2018, decreasing by EUR 0.9 billion compared to the end of March 2017. This year-on-year evolution reflects the normalization of the change in working capital for EUR - 1.1 billion (notably related to temperature effect, margin calls and financial instruments).

By the end of March 2018, the net financial debt / EBITDA ratio at 2.1x is well below the target of ≤2.5x. The Group’s average cost of gross debt slightly decreases compared to end December at 2.53%. The net economic debt / EBITDA ratio stands at 3.6x, improving (5) versus end of 2017 (3.8x).

ENGIE’s successful repositioning

ENGIE is finalizing its transformation plan based on its three programs :

- on the portfolio rotation program (EUR 15 billion disposals net debt impact targeted over 2016-18), the Group has announced to date EUR 13.2 billion of disposals (6) (i.e. 90% of total program), of which EUR 11.6 billion are already closed;

- on the investments program, the whole amount of EUR 14.3 billion (6) growth Capex over 2016-18 is already invested or secured by the end of March 2018;

- regarding the “Lean 2018” performance plan, at end of March 2018, EUR 1.0 billion (6) of cumulated net gains were recorded at EBITDA level. All actions are already identified to reach the target of EUR 1.3 billion savings at the end of 2018.

2018 financial targets

The Group confirms its 2018 financial targets:

- a net recurring income Group share between EUR 2.45 and 2.65 billion. This target is based on an estimated EBITDA between EUR 9.3 and 9.7 billion;

- a net financial debt / EBITDA ratio less than or equal to 2.5x and a maintained “A” category rating;

- a dividend of EUR 0.75/share, in cash, for fiscal year 2018.

The presentation of the Group’s first quarter 2018 financial information used during the investor conference call is available from the Group’s website:

https://www.engie.com/en/financial-results-2018

UPCOMING EVENTS

- May 18, 2018: Shareholders meeting

- May 24, 2018: Final dividend payment (EUR 0.35 per share) for fiscal year 2017. Ex-dividend date is May 22, 2018.

- July 27, 2018: H1 2018 results publication

APPENDIX: Revenues by reportable segment